The Expanding Bullseye: Howden Re’s insights on US population shifts towards vulnerable areas

Over the past 10-15 years, the United States’ population has increasingly shifted towards areas vulnerable to natural disasters. This trend amplifies the effects of the expanding bullseye, a concept highlighting the widening geographical impact of natural catastrophes.

Factors impacting migration towards cat-prone areas

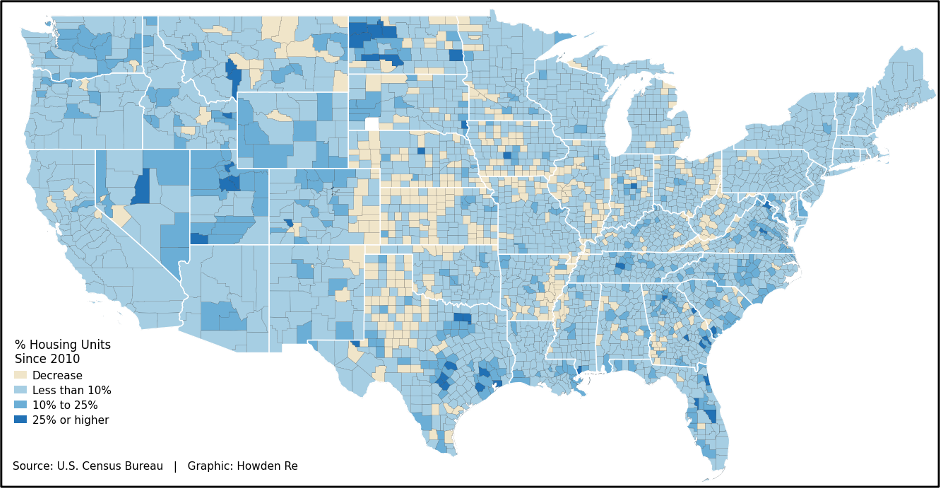

Driven by factors such as affordable housing and the rise of remote work, the nation's urban footprint has expanded significantly, with the number of housing units rising by 17.7% since 2010. Many are drawn by the promise of more land and a perceived higher quality of life, fueling rapid growth in hurricane-prone coastal zones, wildfire-exposed Wildland-Urban Interface (“WUI”) regions, and areas particularly vulnerable to flooding and tornadoes.

US coastal shoreline

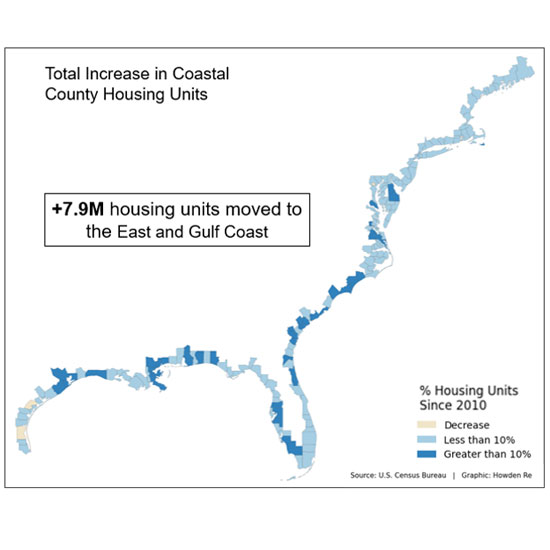

In 2010, approximately 123.3 million people resided in US coastal shoreline counties, accounting for 39% of the national population. From 2010-2020, 7.9 million housing units migrated to Tier 1 counties, those located directly along the Gulf and Atlantic coasts, representing a 13.1% population growth. Hurricane events that might once have affected small populations now strike densely populated areas, leading to costly and widespread impacts. Even with no change to the frequency and intensity of hurricane hazards, more people and assets are at risk of loss.

Swiss Re's Sigma reports are among the most authoritative global sources on catastrophe losses. According to the Sigma reports, the 10-year average of total insured loss is $108 billion, yet in 2024, this figure reached $146 billion, a 35.2% increase. This marks the fifth consecutive year where insured losses have surpassed $100 billion. NOVA, Howden Re's market insight platform aligns with Swiss Re's analysis on the current insured loss trend. Over the last 30 years, insured losses from natural catastrophes have grown at an average annual rate of 5–7%, outpacing global GDP growth.

Swiss Re projects that, if current trends continue, annual insured losses from natural catastrophes could double within the next decade. This projection is based on factors such as increasing asset concentrations in high-risk areas, the intensification of weather-related hazards due to climate change, and rising construction costs.

Severe Convective Storms are now responsible for 40-60% of insured losses, especially in the United States, with increasing frequency of multi-billion-dollar events. On average, only 40-50% of the total economic losses are insured, with a wider gap in developing regions or non-wind perils such as flood or earthquake.

Case Study: The area expansion of Wildland-Urban Interface in California

California's building code requirements for WUI areas, first enforced in 2008, apply to new construction and major remodels in designated Fire Hazard Severity Zones. They mandate fire-resistant materials and design features to reduce wildfire risks. These requirements have been updated in each code cycle, yet older homes do not apply to the new mandates. Between 1990 and 2020, the number of housing units within high-hazard-prone regions of the WUI increased by 20%. The total area of the WUI has expanded by 31% during this same time. These communities often lack the infrastructure, emergency services, and building code requirements needed to withstand major disasters. As such, as more people move in, the potential damage from natural events grows significantly.

As the US continues to develop new areas and people relocate, it is imperative to prioritize the construction of safer, stronger communities. Risk is not solely dependent on location; factors such as building planning, structural integrity, and mitigation efforts also play significant roles, as historic events have shown. For example, when Hurricane Milton impacted the densely populated region South of the Tampa Bay area, losses were lower than originally anticipated, in part due to newer building and repair practices.

Other countries’ adaptation strategies to mitigate the increased population

On the other hand, the Netherlands has managed to stay safe from major floods by using smart planning, strong levees, and systems that help manage excess water. The Netherlands' ‘Room for the River’ initiative is part of the country’s longer-term adaptation strategy aimed at protecting communities built below sea level at a cost of approximately $2.6 billion. From a regulatory perspective and in response to increased flood risk, Germany is expected to introduce requirements for all new and existing residential buildings to have natural hazard insurance. Japan frequently experiences powerful typhoons, but its stringent building codes designed to withstand high winds and flooding have significantly reduced structural damage and minimized business interruption. These resilient construction standards and coverage requirements, regularly updated after major disasters, are a key factor in the countries’ rapid post-storm recovery.

Justin Roth, Associate Director of Catastrophe Analytics R&D, Howden Re, commented: “As the population exposed to climate risk grows, so too should the mitigating efforts. Making resilience part of every step will help protect people and support safer, long-term growth.”

When we look at the increasing cost from catastrophe events, and the 5-7% trend seen in recent years, it is important to account for the impact of changing exposures as one of the key drivers for the growing risk of catastrophe losses to the insurance industry."